Thursday’s earnings call by Billabong for the six months ended 31 December 2017 was its last unless something unexpected happens. With an anticipated late April closing of the acquisition of Billabong by Boardriders for $1.00 a share, with Billabong ending up private, we won’t be seeing any more of the company’s numbers.

Everybody knows that and as a result the call, in a word, was perfunctory. Current CEO Neil Fiske and CFO Jim Howell went through the numbers without some of the usual details, explanations, and nuances. I think there was only one analyst with any questions. I wonder how many even listened.

The discussion was mostly about how tough the market was, why the acquisition had to happen, and the hard things Billabong would have to consider doing if it didn’t close.

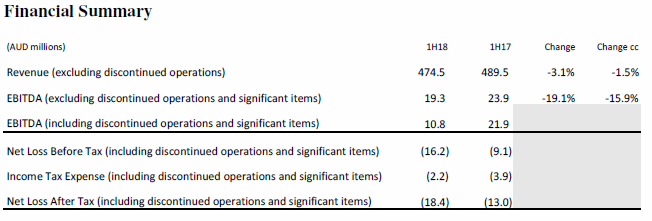

Here’s a summary of the 6 month results:

Note that there are two lines for EBITDA; one including discontinued operations and significant items and one without them. Because there are always, in Billabong’s case anyway, significant items and/or discontinued operations, I tend to focus on the line that includes them. As reported, revenues were down 6.8% to AUD$476.4 million from AUD$511 million.

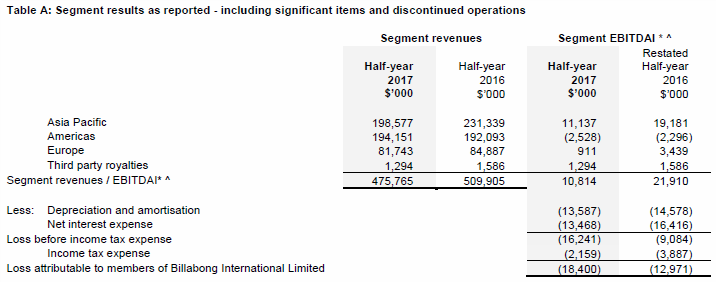

Here are the as reported numbers by segment:

Remember both tables are in Australian dollars.

I’m not going to undertake my usual analysis. I said what I wanted to say when I wrote earlier this week about the document Billabong published discussing the rationale for the acquisition. You can read it here.

Billabong’s efforts to restructure and make its operation more efficient were working. But they were taking too long, and the benefit was offset by revenue declines in a tough market (closing 41 stores, even though it was the right decision, didn’t help). That’s been the story for three or four years. That meant that their balance sheet and financial profile didn’t improve enough to permit the debt to be refinanced. Billabong is also getting 45% of revenue from its retail operations. Retail is not particularly popular in the financial world.

Earlier this week I ended my analysis by saying, “The question is whether the opportunities of two companies in the same tough market improve just because you put them together.” There’s going to be some uncertainty and transitional issues as the synergies (which I believe exist but can’t begin to quantify) are achieved.

Market conditions aren’t going to improve just because Boardriders bought Billabong. Both these companies own brands that suffered some abuse as their owners had financial problems. Becoming private is a good first step towards giving them the flexibility they need to try and rebuild and grow those brands. One wonders if their growth won’t be constrained by the percent of the surf market they already own. Remember what happened to Burton when, already controlling a big chunk of the snowboard market (45%? Just my guess), tried to expand their market share some years ago?

The secret sauce, if it exists, will require 1) patience, 2) great management of distribution, and 3) some subtlety in positioning the brands in the market and against each other. Number three is the hardest and, to me, the most important. A private company can be way more effective than a top line driven public company in doing all three.