SPY’s September 30 Quarter: Not Bad

Last time I wrote about SPY (see it here) in August, they had reported a quarter over quarter sales decline of 18.1% from $10 million to $8.2 million. They told us their largest retail sunglass customer had stopped carrying their brand in the quarter that ended June 30.

But in that quarter’s 10Q they said “The decrease in sunglass sales during the three months ended June 30, 2014 is principally attributable to an overall decline in the consumer market coupled with several key retailers currently holding lower levels of inventory and fewer closeout sales of our sunglass products.”

I was left to wonder whether they had a one-time issue with a big retailer, or a more fundamental problem with the overall market.

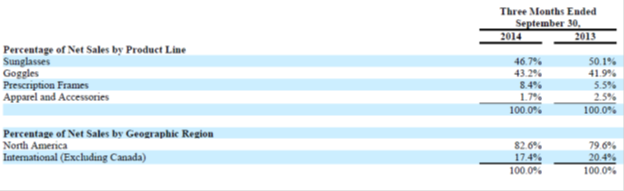

I still don’t know the answer, but the results of the September 30 quarter were improved. Sales rose 8.1% from $10.2 in last year’s quarter to almost $11 million. Below is the breakdown of sales for the quarter by product line and geography. You can see the growth came from goggles and prescription frames. Closeout sales fell from $0.6 to $0.4 million. That’s good to see.

Let me point out a couple of things. The first is the increase in the prescription frames. That’s growth from $558,000 to $922,000 and is approaching 10% of their business. I like that business if only because there are a whole lot of people (like me) who don’t buy sunglasses that aren’t prescription.

Second, note the decline the in sunglasses. It has something to do, I assume, with losing the one big retail account, but may also be just the weak consumer market.

Finally, let’s talk apparel and accessories. Revenues fell from $254,000 to $187,000. Perhaps that’s because SPY has signed an agreement with an unnamed licensee for them to “…develop, introduce, market and sell certain licensed products incorporating SPY IP, including men’s and boy’s apparel, bags and luggage, consumer electronics, protective cases, and other unisex accessories, throughout North America through certain distribution channels, other than deep discount retail channels.”

SPY can’t develop those markets itself so I generally think it’s a good idea depending on just how they define “deep discount retail channels.” You know I think distribution is important where product differentiation is hard to achieve except through marketing, as is the case with many of our industry’s brands.

The gross margin rose from 48.5% to 49.2%. Let me remind you that some of the increase was because the sales to their largest sunglass retailer were lower margin sales. They don’t mention that in the 10Q. They indicate it rose due to lower closeout sales and increased purchases from China.

Total operating expenses rose 7.4% from $4.47 to $4.8 million, but operating income was up anyway from $453,000 to $593,000- 30.6%.

The net loss was only $19,000 compared to $302,000 in last year’s quarter. But their interest expense fell from $756,000 to $612,000 because their major shareholder and debt holder (who are one and the same) chose to reduce the interest rate on about $20 million in debt from 12% to 7% during the previous quarter. That explains $144,000 of the improvement.

Okay, let’s talk balance sheet. Net accounts receivable were almost unchanged. In fact they fell by $14,000 to $6.53 million. But trade receivables, before allowances for returns and doubtful accounts rose from $8.54 to $8.92 million. Not a big deal given the sales increase. But the allowance for returns rose from $1.63 to $2.07 million, or by 27%, and I wonder what’s going on there. Maybe nothing. I just wonder what kind of deals they are making.

Inventories were up 28% from $5.87 to $7.53 million. Seems like a big increase, but that could just be a timing issues if goggles to be shipped for this season showed up a bit early.

Current ratio fell from 1.73 to 1.40. I note that cash provided by operations during the nine months of the year declined from a positive $2.49 million to a negative $53,000. This is due to “…timing of seasonal goggle purchases [so, as suspected, this has something to do with the inventory increase], interest payments on related party debt, and a decrease in sunglass sales. During the year ended December 31, 2013, the Company had positive cash flow from operations principally as a result of a significant reduction in operating expenses, an increase in gross profit, and by paying interest in kind.”

I’ll remind that you the agreed upon reduction in the interest rate included a provision that interest would now be paid in cash rather than accrued as more debt.

So SPY had a pretty good quarter. But improvements from expense reduction are probably over. Perhaps we can hope for some further improvement in gross margin through increasing Chinese production. The sunglasses business grew slightly to $5.13 million. The increase was only $40,000 which may be a good or a bad result depending on just how many dollars losing the one big retail customer cost them. Sunglasses are a tough business.

Leave a Reply

Want to join the discussion?Feel free to contribute!