Billabong’s Six Month Report: The More Things Change, the More They Stay the Same

Six months ago, reporting on Billabong’s results for the whole year, I said this was a challenging turnaround, Billabong was doing things right, they were starting to see results, but the market was tough, and implementing their plan was taking longer and costing more (perhaps because it’s taking longer) than they’d initially expected.

That’s all still true for the six months ended December 31, 2016.

I’ll start with the numbers as reported (numbers in Australian dollars).

Total revenue fell 9.6% from $565 million in the six months ended December 31, 2015 (the prior calendar period-PCP) to $511 million in the six months ended December 31, 2016. The gross profit margin declined from 52% to 50.9%. Selling, general and administrative expense fell 10.2% from $219 to $196 million.

Other expenses fell from $61 to $59 million. Financing costs were down a bit from $19.5 to $18.6 million.

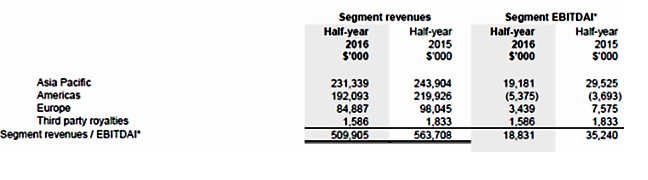

Income tax expense rose slightly from $3.7 to $3.9 million and net income declined from a loss of $1.59 million to a loss of $16.1 million. Here’s the revenue and EBITDA as reported by region. As you can see, all three segments took a hit in revenue and EBITDAI.

I will remind you that revenue was impacted by the sale of Sector 9. Billabong had to keep it in their reported results because of its small size (rather than show it as discontinued). They tell us in their presentation that in constant currency revenues fell just 5.8% after taking Sector 9 into account. There’s also a note that in the PCP, Sector 9’s EBITDAI was a negative $1.1 million.

There was also some revenue reduction because of store closings. We’ll see further reductions in revenue resulting from sales of other, small brands.

Honestly, I’m not that concerned about a certain amount of revenue reduction at this point, though of course, I don’t have to manage a public company and explain it to analysts who do care (though only one analyst had any questions on the conference call). Some caution in managing your distribution as a tool for improving your brand positioning is a good thing, even if it leads to some amount of revenue decline. And I continue to agree with their decision to focus on theirs three large brands and sell their small brands, if only because their balance sheet requires it.

Which brings us to the sale of Tigerlily, even though that’s a second half fiscal 2017 item. I want to talk about it in terms of Billabong’s balance sheet, which had borrowings of $280 million at the end of the year, up from $275 million a year ago.

Tigerlily is the most profitable of Billabong’s smaller brands. Calendar year 2016 revenues were $29.6 million. $18.8 million of that amount was in the six months ended December 31, 2016. During those six months, it had an EBITDA of $5.5 million. $7-8 million is projected for the entire fiscal year.

When the sale closes, those revenues and income go away. But the selling price is $60 million, and that will make a bunch of debt go away. The pro-forma adjustment for December 31, 2016 shows gross debt declining from $286 million to $230 million, a 20% decline. That means a decline in annual interest charges. Remember this is a company that reported a loss for six months of $16 million and finance costs of $18.6 million.

As CFO Pete Myers put it, “The Tigerlily sale is an important step towards putting us in a position to consider our refinancing options. But an even more important step is delivering on the earnings improvements we’ve outlined in the second half. Then we can begin to explore the market to see whether there are options that represent a meaningful improvement to our current deal.”

Debt repayment, and refinancing at a lower rate when they can do it, will have a very positive impact on Billabong’s bottom line.

As long as we’ve wandered to balance sheet issues, I guess we might as well finish checking it out. The current ratio rose from 2.3 to 2.4 even in the face of a 28% reduction in cash and cash equivalents compared to a year ago. Receivables rose 3.8% to $137 million, which I guess you’d prefer not to see as revenues decline. Inventories, however, fell 14.3% to $186 million. The current ratio improved as current liabilities declined 18.4% as Billabong paid down its trade and other payables. This is from consolidating their supplier base- a very good thing. Equity fell from $281 million a year ago $242 million.

Cash flow from operating activities for the half year increased to $27.3 million from $12.3 million in the PCP. That’s good to see. I will look forward to balance sheet improvement as other small brands are sold and as operating performance improves.

With the balance sheet detour complete, let’s get back to operating results.

As usual, Billabong wants you to know that they had some “significant items” that they think you might want to exclude in evaluating their results. I don’t know- it seems to me that if they were “insignificant” you might want to exclude them but why would you ignore stuff that’s significant?

The total for the current six-month period was a pretax expense of $10.5 million. In the PCP it was a pretax expense of $2.0 million. The result is an adjusted EBITDAI for the whole company of $29.3 million in the current period and $37.2 million in the PCP. You can look above and compare that with their as reported EBITDAI.

I have no idea how you can ignore a $5 million inventory adjustment (the largest adjustment), but here’s how they explain it.

“During the period, an adjustment to inventory was required as part of a continuous improvement project that the Group undertook to improve the accuracy and consistent application across the Group of costing and valuation methodologies. This resulted in an adjustment to United States of America and Canada inventory of $5.0 million relating to prior periods.”

Oh- I see. Their EBITDA from some earlier period of periods is overstated by $5 million, but they are taking the adjustment in this period. But because they are taking in this period, rather than going back and restated their financial statements, we should ignore it. This is brilliant! Not only didn’t they take the $5 million charge in past periods when they should have, but they are not telling us not to pay any attention to it now when they take it?!

I better move on. This can’t be good for my blood pressure.

Let’s talk about something a little more fulfilling, like brands and branding. In the presentation that went with the conference call we learn that 88% of their wholesale business came from their big three brands. 50% was Billabong. Element and RVCA were each 19%. That leaves 12% of wholesale for all the other brands.

CEO Neil Fiske, in his conference call remarks, that “The key measures of brand equity are mostly up.” Obviously, that’s good news, though I would have minded a little more specificity. At the end of the day, if your brands aren’t strong, you don’t have a business.

He goes on to say later, “Turning to our brands, we faced challenging trading conditions across each of our markets, however our brands more than held their own competitively with important share gains and growing followership around the globe. Our brands, our athletes and advocates have collectively more than 34 million followers on social media, up 33% on prior year. There’s tremendous value to be unlocked from this direct relationship we are building with this highly engaged follower base.”

What’s the best way to get that growth in followers to translate into higher revenues? We’re all trying to figure that out.

The varied, numerous, and necessary “Platform Initiatives” Billabong is undertaking continue to be implemented. The presentation lists 22 of them. Except as to how it impacts cash flow, I’m not dismayed by some delays that have popped up. As I’ve said before, it’s kind of like trying to change the oil in your car while driving it. They are doing the right things for the right reasons. Over time, I expect better results they are publicly suggesting.

Billabong is projecting a stronger second half, with higher comparable gross margins and costs and inventories in better shape.

I’m going to make this shorter than my usual Billabong reviews. I have the troubling feeling that when I wax loquacious for 2,500 words, nobody reads it anyway.

The conference call presentation listed four factors to explain the EBITDA result. They revolved around issues with weather, currency, and an order drop from a distributor.

I largely believe in Billabong’s strategy. That doesn’t mean I know it will succeed, but I think it’s what I would have done. I would much rather be told that some things we’re doing are taking longer and costing more and we’ve got more work to do brand building then that it’s the currency, the weather, and a customer surprise. It will always be the currency and the weather and some customer doing something unexpected. We never have any control over those. Branding, systems, and organization, on the other hand, are things Billabong can sink its teeth into.

Leave a Reply

Want to join the discussion?Feel free to contribute!