Retailer Plans to Go Public. Wait…Now?…A Retailer?…Really?

Roots, a Canadian retailer, has filed a prospectus for a public offering. Here’s the link to their web site. As usual, the initial prospectus is missing a lot of key numbers, but I’ll do the best I can.

Roots has been around since 1973, so they must be doing something right. “As of July 29, 2017, our integrated omni-channel footprint included 116 corporate retail stores in Canada, 4 corporate retail stores in the United States, 109 partner-operated stores in Taiwan, 27 partner-operated stores in China and a global e-commerce platform that shipped to 54 countries during our most recently completed fiscal year.” They had 2,200 full time employees.

Here’s how they describe their brand and market position.

“…we are an inclusive lifestyle brand for those who want to enjoy the moment and embrace the spirit of the open air. Our products are worn by a broad cross-section of global consumers, including young professionals, students, families, athletes and entertainment icons. For nearly five decades, people have been drawn to the timeless style, comfort, functionality and versatility of our products and the stories and experiences that have shaped our brand. Canada will always be at the heart and soul of our business, but our guiding principles and premium products that this country has inspired transcend borders.”

That comes a little too close to saying, “We can sell our products to anybody anywhere.” I don’t think that’s ever the case, but they’re trying to get people to invest, so I guess we can forgive a little hyperbole.

I like their high-end leather products (they’ve got their own leather factory in Canada). I guess I can see the Canadian ethos through the whole product line. I admire the consistency with which they’ve pursued a strategy over decades. Oh- and they make money. I like that too.

Here’s what they list as their five competitive strengths:

- Iconic Canadian brand with rich heritage.

- Diversified product portfolio with enduring icons.

- Broad demographic appeal with strong loyalty.

- Connective omni-channel experience.

- Experienced and passionate management team.

Except for being a Canadian brand, most other retailers would like to claim the same strengths. I’m never quite comfortable when your advantage is supposed to come from doing the same things others are doing, only doing them better.

Meanwhile, there growth strategies are:

- Leverage operational investments.

- Pursue continued growth in Canada.

- Develop footprint in the United States.

- Expand in international market.

- Deepen our offering in leather and footwear.

Once again, we see a lot of trying to do what everybody else is trying to do. The Canadian growth strategy focuses on ecommerce, but I have to wonder how many brick and mortar stores they think Canada can ultimately support.

As an example, let’s dig one layer deeper on their plans to grow in Canada. They plan to do that by:

- Amplifying our brand communication.

- Leveraging our United Brand Range.

- Optimizing our stores.

- Enhancing our e-commerce platform.

Each of these is in turn described in more detail, but at the end of the day are they going to be able to do them better than the competition?

I like their guiding principles of self-confidence, authenticity, quality and integrity a lot better. An organization where there’s consensus around those four things should be an effective one that would know where to focus its time and what was “right” and “wrong” for the company. A set of principles like that is both empowering and guiding.

They also have comfort, Canadiana, open air and experience as their four distinct marketing themes. “We use these four themes to thoughtfully cater to local market demographics, depending on whether our stores are located in urban centers, student towns or targeted tourism gateways. With this approach, we are able to curate our offering to the specifics of each local market and customer profile in order to maximize store sales and profitability.” I can see value there.

But I still can’t get past the “me tooness” of their competitive strengths and growth strategies. To invest in Roots, you have to believe their history, guiding principles, and marketing themes makes it credible that they can do the same things their competitors are doing but do them better. They come across sounding disciplined and focused, but so do some of their competitors.

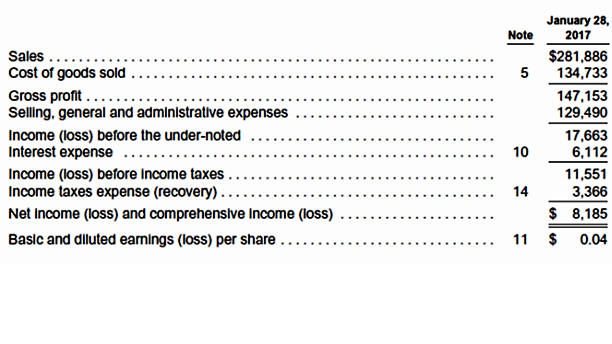

Inevitably, we find our way to the numbers. We’ve got three and six-month periods, projections, full year statements, predecessor and successor financials, and adjusted EBITDA numbers. They are required to provide all this in the prospectus, but it doesn’t make for easy reading or analysis. But you know me- I’m disdainful of too many “adjustments.” So, I’ll head right off to the audited financials (all numbers in Canadian dollars).

Oops, there’s a problem The audited numbers are for the years ended January 30, 2016 and 2017 and the revenue numbers for the two years are $61 and $282 million respectively. It seems the company going public (Roots Corporation) was formed on October 14, 2015 and then, on October 21, acquired all the assets that make up the current business effective December 1, 2015. Hence, the big difference in revenue.

This is a bit of a conundrum. I don’t have two full years to compare- audited or otherwise. I guess we’ll take a look at the audited statements for the year ended January 30, 2017 and go from there.

The gross margin is 52.2%. As I said, I don’t have a previous year to compare to, but there is a bit of information in the notes.

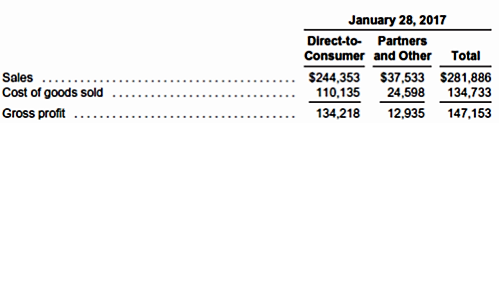

Direct to consumer revenues are their owned retail stores and ecommerce in the U.S. and Canada including all ecommerce. The partner and other numbers are wholesale and royalty income from the stores in the Far East. Excluding the Far East business, the gross margin is 54.9%.

The balance sheets for January 30 and 28 for 2016 and 2017, respectively, are comparable, so let’s take a look at them.

Year over year, cash has risen from $8.5 to $25.3 million. Inventory has fallen 14.8% from $38.4 to $32.7 million. Hard to put that in context when we don’t have comparable sales data.

The current ratio is a little better than 2 to 1, slightly better than a year ago. The noncurrent liabilities are up slightly to $156 million. I’d note that those include $99 million of long term debt. Interest on that debt was $5.4 million during the year, up from $978,000 in the previous year. Those numbers aren’t comparable because of the acquisitions.

$5.5 million of this term loan has to be paid off during the year following the balance sheet date. The next four years require payments of $7.6, $8.3, $10.4 and $74.9 million respectively. Total equity of $201 million is up from $192 million at the end of the previous year.

This is probably the right place to let you know that all the proceeds of the public offering will go to the selling shareholders. Not a cent comes to the company to finance the growth it has planned or to pay down debt. Good for the shareholders and I hope they pull it off, but if I were a potential investor, which I’m not, finding that out would make me flee into the night.

I was going to look at the year to date and numbers for the second quarter, but I don’t think I’ll bother. They lose money, but seasonality means they only do 30% of their business during the first two quarters, so that’s expected. Year over year, both year to date and in the second quarter sales are up and the loss has declined.

I could analyze the numbers they provide forever. But I can’t get around the contradiction of their growth plans and debt repayment juxtaposed against the fact that none of the offering proceeds are going to the company. And in spite of their longevity, and some insightful guiding principles and marketing themes, I get nervous when somebody’s strategy is to do the same things others are doing, but do them better.

I will be interested to see if they get this done. And if they do, I’ll be the first to congratulate the selling shareholders on their liquidity event.

Leave a Reply

Want to join the discussion?Feel free to contribute!