When a smaller company in our industry is acquired by a conglomerate, it often becomes difficult to follow how the acquired company is doing because the conglomerate isn’t required to release any details on that company’s performance. Think Reef after it was acquired by VF (though I imagine we might have heard more if Reef had been doing better).

PPR, however, is telling us a bit about what’s going on with Volcom and its plans for the Sports & Lifestyle segment of which Volcom is a part.

PPR is a French company with revenues of 9.7 billion Euros in the year ended December 31, 2012. The current exchange rate is about $1.3 to the Euro. So 9.7 billion Euros is around US$ 12.6 billion. It acquired Volcom in July of 2011.

PPR has two divisions; its Luxury Division and Sport & Lifestyle. PPR’s luxury brands, including Gucci, Bottega Veneta, and Yves Saint Laurent, contributed 64% of its revenue for the year, or 6.2 billion Euros. The remainder (3.532 billion Euros) came from its Sports & Lifestyle segment that includes Volcom and Electric as well as Puma, Cobra (golf) and Tretorn (outdoor footwear).

The last complete fiscal year results for Volcom we saw before it was acquired was for the year ended December 31, 2010. In the complete year, in US dollars, Volcom reported revenue of $323 million. Operating income was $30 million net income $22 million. Keep those numbers in mind as we move forward.

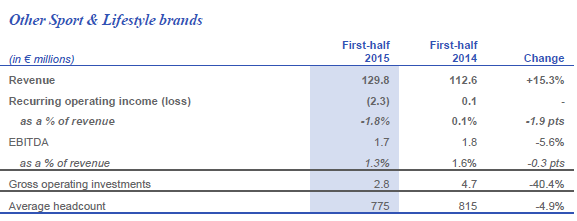

Of the total Sport & Lifestyle segment, Puma revenue represented 3.271 billion Euros, or 92.6% of the segment’s total. That means that Volcom, Electric, Cobra and Tretorn collectively generated revenue of 261 million Euro. You can see that result on page 27 of this PPR document. Go ahead and look just so you know I’m not making it up.

At 1.3 Dollars to the Euro, that’s about US$ 339 million. That’s only 2.7% of PPR’s revenue for the year, so it’s not really significant financially.

There is a bit of confusion here. Page 40 of the full financial result (which you can down load here (It’s the first item on the list after you click “documents” at the top) talks about “Other Brands” in the sport and lifestyle segment. That is, all brands in that segment except Puma. It specifically lists Volcom and Electric (but not the other brands) and says they had revenue of 261 million Euros and recurring operating income of 15 million Euros. But it seems to exclude Cobra and Tretorn.

I can’t tell, then, if the 261 million Euros in 2012 revenue is just Volcom and Electric or includes these other two brands. I suspect that it does.

Compare those numbers for Sport & Lifestyle segment excluding Puma with Volcom’s numbers in its last year as a public company. Note that operating income is US$ 19.5 million and is a third less than Volcom’s stand-alone operating income in its last full independent year. At best, Volcom has grown only a bit. If that 261 million Euros in revenue includes Cobra and Tretorn, Volcom’s year over year revenues could have fallen. In the fourth quarter, according to the financial report, Sport & Lifestyle revenues rose 7.6% on a comparable basis. But excluding Puma, comparable segment revenues were down 4.8% and totaled 64 million Euros. As far as I can tell Volcom (including Electric) is most of what’s left in the segment after you remove Puma.

I would like, at this time, to renew my congratulations and admiration, expressed at the time of the deal, to the Volcom management team for the timing of their sale to PPR and the price they got.

In the conference call, we learn that Volcom held its gross margin, but that marketing initiatives had a negative impact on operating margin. PPR management also referred to a “…worsening economic context…” and a “…major reorganization of certain retailers, notably in the United States…” in the second half of the year.

Puma’s recurring operating income for the year was down 13% while that of the other sport and lifestyle brands rose 9.6%. EBITDA fell 10.5% for Puma but rose 28.1% for the Sport & Lifestyle segment. Remember most of the improvement in the other Sport & Lifestyle brands results from owning Volcom for a whole year. Impossible to tell what they would have been without that.

In spite of the rising sales Puma’s net income fell from 230 million Euros in 2011 to 70 million Euro in 2012. PPR is implementing a Transformation and Cost Reduction program for Puma. This will involve clarifying brand positioning, improving product momentum, improving efficiencies in the value chain and revamping the organization. Apparently, the organization didn’t evolve as the brand grew and that caused some problems. I’d note that as this program of transformation and cost reduction proceeds, average head count at Puma has risen from 10,043 in 2011 to 10,935 in 2012.

It’s also interesting to see that for the year wholesale revenues, which accounted for 81.6% of Sport & Lifestyle revenue, grew by only 0.6%. We’re told, “The unsettled economic environment in Western Europe, coupled with the reorganization of Volcom’s distributor store networks in North America, weighed on the performance of this distribution channel during the year.” Retail sales in directly operated stores (don’t know if that includes online) rose 17.6%.

In the conference call, we were told that more Sport & Lifestyle acquisitions were expected after Puma had been turned around and that there would be a focus on outdoor. Puma is to remain the core of the Sport & Lifestyle segment.

Here’s what PPR wants to do with its Sport & Lifestyle brands:

“For its Sport & Lifestyle brands, PPR’s strategy is based on expanding into new markets while bolstering

growth in the most mature ones, developing distribution, launching new products that are consistent with each brand’s DNA, and continuing to identify and foster synergies between the brands, particularly in sourcing, logistics and knowledge sharing in the areas of product development, distribution and marketing. The objective is to regroup sports brands that have an extension into Lifestyle.”

There’s nothing wrong with that but it’s kind of generic and pretty much lists what all brands want to do. But as I’ve noted before, that’s all you can expect in a public document. No company wants to lay out its strategy in detail for its competitors.

While Puma struggles and it’s not clear that Volcom is doing all that well, PPR management is looking at revenues from their Luxury Brands that grew 26.3% year over year, while Sport & Lifestyle was up only 11.9%. Recurring operating income from Luxury was up 27.6% but fell 12.1% in Sport & Lifestyle. EBITDA rose 26.6% in Luxury, but fell 9% in Sport & Lifestyle.

It’s enough to make a management team schizophrenic. The Luxury Brands that represent two thirds of your revenue are doing great. Sport & Lifestyle, where you obviously see potential and opportunity (or you wouldn’t have bought Volcom) aren’t doing so well. But you expect to make further acquisition in this segment and have an outdoor focus.

We’re only a year and a half from the acquisition of Volcom, and that isn’t long to integrate a company and bring the strengths of PPR to bear. Puma has obviously helped Volcom introduce its new shoe line. But Puma and Volcom seem to me to be very differently focused companies. And as I think about outdoor, I’m not sure that’s how I think of either of them.

When PPR bought Volcom, I suggested, kind of half seriously, that maybe PPR would turn Volcom into an upscale, boutique kind of brand and develop some appropriate products. I’m now up to maybe two-thirds serious about that.

PPR no doubt has noticed that everybody is interested in the youth culture and outdoor markets and think they should be too. Can’t blame them. But I come away from their documents and conference call with the sense that they maybe they aren’t quite clear on what the sport/lifestyle/outdoor market represents.

During the conference call, between the presentation and the question and answer session, there was a short video featuring flashes of most of their brands. There was a lot of action sports material in it. But occasionally when the skate or snowboard trick was bracketed with the golf shot, it felt like there a certain discontinuity in the whole thing. Maybe I’m reading too much into that, and it was perfectly appropriate for the audience. But I think PPR knows that they need to think about how the brands in their Sport & Lifestyle segment are positioned and, ultimately, why they are in the business if they can’t get growth and returns consistent with their luxury brands.