As I just noted in my last post on Tilly’s and expect to note as I get to other retailers, the teen market is sort of lousy right now. People seem a bit perplexed as to why it’s fallen so hard, but I believe it’s as simple as a lack of money and jobs for teens. And I suppose I’d add a lack of product differentiation and very broad market with way too many competitors and retailers.

A & F’s results for the year reflect that and some of their responses are interesting, though consistent with what other retailers are doing. But remember that, unlike many retailers they compete with, they only sell their own brands. Let’s start with the numbers after which it will be easier to explain their reaction to market conditions.

The Results

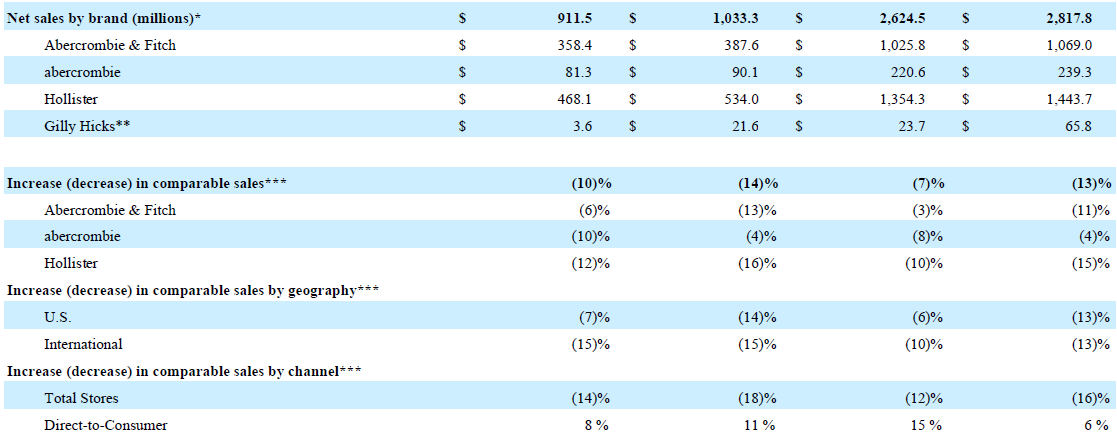

Net sales for the year ended February 2, 2013 declined 8.7% from $4.51 to $4.12 billion. Be aware that 2012 had a 53rd week in it, which happens from time to time. That’s about a $63 million difference caused by the extra week. Below are the sales by brand and geography for both years.

You can see that most of the sales decline was in the U.S. and split between the Hollister and Abercrombie & Fitch brands. Gilly Hicks stores are by now all closed, though certain of the product is going to be sold in their other stores. Total Hollister sales, including direct to consumer, were down 14%. Abercrombie & Fitch fell by 10%.

Note that the U. S. stores delivered sales of $2.16 billion and operating income of $195 million. The international stores had sales of $1.18 billion and operating income $249 million. And direct to consumer’s revenues of $777 million generated operating income of $295 million. Of the three segments, guess which two they will be focusing on.

Here’s what they say about online sales. “Total net sales through direct-to-consumer operations, including shipping and handling revenue, were $776.9 million for Fiscal 2013, representing 19% of total net sales. The Company operates 46 websites including both desktop and mobile versions. In addition, the websites are available in nine languages, accept seven currencies, and ship to over 120 countries.”

Like other retailers, they are big on the omnichannel, and are enthusiastic about growing online business. And, like other retailers, they really don’t talk about whether said online sales are incremental or taking away from brick and mortar sales. That to me is the big question nobody seems to be addressing publically. Amazing the analysts don’t ask. Especially since brick and mortar comparable store sales fell 16% during the year while direct to consumer was up 13%.

The company ended the year with 843 stores in the United States and 163 stores outside of it for a total of 1,006. That’s down from 1,041 at the end of the prior year. They opened 24 international stores but closed a net of 59 in the U.S. 21 of the closed stores in the U.S. were Hollister. They expect to close 60-70 stores in the U.S. during 2014. They’ve got 500 leases expiring between now and 2016 so they’ve got a lot of flexibility in term of what they do with existing stores.

Gross profit at 62.5% was up just one 0.1%. Store and distribution expense went down a bit from $1.981 to $1.908 billion but as a percentage of sales rose with the sales decline from 43.9% to 46.3%. Marketing, general and administrative expense rose from $474 to $482 million. As a percentage of sales, it was up from 10.5% to 11.7%.

To add to the fun, there were restructuring charges of $81.5 million and asset impairment charges of $47.7 million. That was offset a bit by $23 million of other operating income. The $81.5 million was for closing the Gilly Hicks stores.

Operating income got whacked by the double whammy of lower sales and higher charges, falling 78% from $374 to $81 million. Net income for the year was down a similar 77% from $237 to $55 million.

Fourth quarter sales were down 11.5% to $1.3 billion. The quarter’s gross margin was down 4.4% from the same quarter in the prior year. We learn in the conference call that the decline “…reflected an increase in promotional activity during the high volume holiday season, including shifting promotions in the direct-to-consumer business and an adverse effect from the calendar shift.” Net income fell from $157 million in last year’s quarter to $66 million in this year’s. Note that net income for the whole year was $55 million.

The balance sheet is fine, with a current ratio that’s improved though equity has fallen in spite of still earning a profit from $1.82 to $1.73 billion. I’m particularly interested to see inventory rise 24.4% from $427 to $530 million while sales fell. I would note that the reserve for inventory at February 1, 2014 was $22.1 million, up from $9.9 million a year ago. They remind us that inventory is down 22% from two years ago.

Cash at year end is down slightly from $643 to $600 million. There are also some borrowings of $135 million of which there were none last year. Cash provided by operating activities took a tumble, falling from $684 to $175 million.

Okay, here’s a fun financial fact. During the year they spent $115.8 million to buy back their own common stock. In addition, in March 2014 they entered into an Accelerated Share Repurchase Agreement with Goldman, Sachs & Co., paid them $150 million, and received 3.1 million shares of A & F common stock. There will be some more shares bought under the agreement.

Here’s what CEO Michael Jeffries said about that:

“Our capital allocation philosophy remains to return excess cash to shareholders. To that end, on February 27, we entered into a $150 million accelerated share repurchase agreement pursuant to the existing open share repurchase authorization of 16.3 million shares. The accelerated share repurchase agreement reflects our confidence in our ability to achieve significantly improved performance and create sustainable value for shareholders. We anticipate additional share repurchases over the course of the year, utilizing free cash flow generated from operations in addition to utilizing existing or additional credit facilities.”

Okay so I’m confused. I’m not a shareholder but if I heard that I’d probably ask Mr. Jeffries why he didn’t just pay me a dividend. I know the concept is that reducing the shares outstanding increases the share price, but I don’t think shareholders feel any “excess cash” in their pockets as a result of the share buyback. And I might wonder how many shares had been issued to executives and other employees in the form of options or grants and the extent to which that offset the buy back. I might even wonder why it was that the company couldn’t find anything better to do to with that cash to increase the value of my shares. And I wouldn’t just wonder that for Abercrombie & Fitch, but for a whole bunch of other companies.

A little off the topic, but an interesting thing to think about.

Issues of Strategy

Under the Long Term Strategic Plan section of the 10K, A & F tells us their priorities to improve operating margins:

• Recovering productivity and profitability in our U.S. stores

“…we are focused on continuing to improve our fashion, particularly in our female business, and increasing brand engagement. We are taking steps to evolve our assortment, improve our product test capabilities, shortening lead times and increasing style differentiation across all classifications. In addition, we will be launching global marketing campaigns….While we expect that a number of initiatives will improve average unit retail over time, we believe we will need to be more competitive on average unit retail in the current environment and will look to aggressively reduce merchandise average unit cost in order to give us that flexibility.”

• Continuing our profitable international growth

They will be focused on Japan, China and the Middle East and would like to see international reach 50% of revenues. They don’t say by when.

• Increasing direct-to-consumer penetration

They’d like to see that be 25% of sales.

• Reducing expense

They’ve got programs in place to reduce costs by $175 million on an annualized basis, though that will be offset by $30 million in new marketing programs. They don’t say this, but I wouldn’t be surprised if the program includes some consolidation of vendors. They note that they’ve got more than 175 vendors, none of which made more than 10% of their product. As described above, their online presence also seems a bit complicated, and I can imagine some consolidations of their web sites as well.

• Maintaining capital expenditures at approximately $200 million

• Returning excess cash to shareholders

This is where they further discuss their share buyback program. You already know how I think about that.

A lot of this seems like goals rather than strategies to me. And, as I’m finding myself saying for most every retailer I review, they don’t seem particularly different from their competitors.

They go on to describe how important their employees are in creating the store atmosphere and how they are “evolving” their consumer engagement strategy “…to further develop leading digital experiences.”

They note that the in-store experience “…is still viewed as a primary means of communicating the spirit of each brand.” Not “the” primary means but “a” primary means. Well, just how does mobile and online interface with brick and mortar? We’re all going to find out how that works together.

And, correctly in my judgment, but once again like pretty much everybody else, A & F “…continues to invest in technology to upgrade core systems to make the Company scalable and enhance efficiencies, including the support of its direct-to-consumer operations and international expansion.”

A & F, you need to remember is different from other retailers in our space as all their product is their own brands. If those brands are strong enough, that’s a major point of differentiation and competitive advantage. But it requires spending marketing dollars on brand building in excess of what other retailers have to spend. I noted above that they are going to spend more marketing dollars this year.

Then of course there’s the minor problem that if a brand isn’t working out, you can’t just say, “Screw it, let’s go get another brand” like retailers who sell third party product can do. Recognizing this, A & F announced during the conference call that they are “…looking at selling third party brands through our channels and selling our branded merchandise through third party channels.” They don’t give any details.

If this happens, it will be very interesting to watch. I’m wondering what channels would carry Abercrombie & Fitch or Hollister and what impact that will have on consumer perception of the brand. I have a hard time imaging Zumiez, just to pick an example, carrying their brands. Why would they help validate the brands of a competitor?

And then I wonder why an established brand would want to be in a Hollister store where 80% of the merchandise, to pick a number, would still be Hollister. I’m not against this. I don’t even think it’s necessarily a bad idea and I applaud A & F for thinking some out of the box kinds of thoughts. I’ll be interested to see what the details are and how it works out.

Management also talked about the Hollister brand moving more towards fast fashion, and its average unit retail (AUR) price coming down. They talk about the competitive environment that requires it. CEO Jeffries put it’s like this:

“We think that the opportunity in AUC reduction is in the Hollister brand, and we think that we have an opportunity to reengineer some of that product, take some costs out of the products, which is still maintaining the quality level that is appropriate for that customer and that brand. Most of the cost initiatives will come from Hollister. But as we compare A&F for the rest of our competition, and Hollister, as we are looking at that brand and who the core customer is, we will be better quality than the competition, but there will be some reengineering of that product.”

There’s a lot going on at A & F. Much of it is consistent with what other retailers are doing. Like all of the teen retail space, A & F is having to be reactive in a hard market. As it always does, a strong balance sheet will help them. I’m intrigued by how carrying other brands and offering their own brands to other channels will work out. Not doing that has been a source of differentiation for the company and has given them some control of brands that other retailers don’t have. It’s a big change, and for it to meaningful it may be hard to do just a little. The devil, as they say, is in the details. But as I’ve always encouraged risks, thinking that doing nothing is the biggest one, I’m pretty much for trying it.